Register now or log in to join your professional community.

Statement of Changes in Equity, often referred to as Statement of Retained Earnings in U.S. GAAP, details the change in owners' equity over an accounting period by presenting the movement in reserves comprising the shareholders' equity.

Movement in shareholders' equity over an accounting period comprises the following elements:

Following is an illustrative example of a Statement of Changes in Equity prepared according to the format prescribed by IAS 1 Presentation of Financial Statements.

ABC PlcStatement of changes in equity for the year ended 31st December 2012 Share Capital Retained Earnings Revaluation Surplus Total Equity USD USD USD USD Balance at 1 January 2011 100,000 30,000 - 130,000 Changes in accounting policy - - - - Correction of prior period error - - - - Restated balance 100,000 30,000 - 130,000 Changes in equity for the year 2011Issue of share capital - - - - Income for the year - 25,000 - 25,000 Revaluation gain - - 10,000 10,000 Dividends - (15,000) - (15,000) Balance at 31 December 2011 100,000 40,000 10,000 150,000 Changes in equity for the year 2012 Issue of share capital - - - - Income for the year - 30,000 - 30,000 Revaluation gain - - 5,000 5,000 Dividends - (20,000) - (20,000) Balance at 31 December 2012 100,000 50,000 15,000

165,000

Components

Following are the main elements of statement of changes in equity:

Opening Balance

This represents the balance of shareholders' equity reserves at the start of the comparative reporting period as reflected in the prior period's statement of financial position. The opening balance is unadjusted in respect of the correction of prior period errors rectified in the current period and also the effect of changes in accounting policy implemented during the year as these are presented separately in the statement of changes in equity (see below).

Effect of Changes in Accounting Policies

Since changes in accounting policies are applied retrospectively, an adjustment is required in stockholders' reserves at the start of the comparative reporting period to restate the opening equity to the amount that would be arrived if the new accounting policy had always been applied.

Effect of Correction of Prior Period Error

The effect of correction of prior period errors must be presented separately in the statement of changes in equity as an adjustment to opening reserves. The effect of the corrections may not be netted off against the opening balance of the equity reserves so that the amounts presented in current period statement might be easily reconciled and traced from prior period financial statements.

Restated Balance

This represents the equity attributable to stockholders at the start of the comparative period after the adjustments in respect of changes in accounting policies and correction of prior period errors as explained above.

Changes in Share Capital

Issue of further share capital during the period must be added in the statement of changes in equity whereas redemption of shares must be deducted therefrom. The effects of issue and redemption of shares must be presented separately for share capital reserve and share premium reserve.

Dividends

Dividend payments issued or announced during the period must be deducted from shareholder equity as they represent distribution of wealth attributable to stockholders.

Income / Loss for the period

This represents the profit or loss attributable to shareholders during the period as reported in the income statement.

Changes in Revaluation Reserve

Revaluation gains and losses recognized during the period must be presented in the statement of changes in equity to the extent that they are recognized outside the income statement. Revaluation gains recognized in income statement due to reversal of previous impairment losses however shall not be presented separately in the statement of changes in equity as they would already be incorporated in the profit or loss for the period.

Other Gains & Losses

Any other gains and losses not recognized in the income statement may be presented in the statement of changes in equity such as actuarial gains and losses arising from the application of IAS 19 Employee Benefit.

Closing Balance

This represents the balance of shareholders' equity reserves at the end of the reporting period as reflected in the statement of financial position.

Purpose & ImportanceStatement of changes in equity helps users of financial statement to identify the factors that cause a change in the owners' equity over the accounting periods. Whereas movement in shareholder reserves can be observed from the balance sheet, statement of changes in equity discloses significant information about equity reserves that is not presented separately elsewhere in the financial statements which may be useful in understanding the nature of change in equity reserves. Examples of such information include share capital issue and redemption during the period, the effects of changes in accounting policies and correction of prior period errors, gains and losses recognized outside income statement, dividends declared and bonus shares issued during the period.

Components

Following are the main elements of statement of changes in equity:

Opening Balance

This represents the balance of shareholders' equity reserves at the start of the comparative reporting period as reflected in the prior period's statement of financial position. The opening balance is unadjusted in respect of the correction of prior period errors rectified in the current period and also the effect of changes in accounting policy implemented during the year as these are presented separately in the statement of changes in equity (see below).

Effect of Changes in Accounting Policies

Since changes in accounting policies are applied retrospectively, an adjustment is required in stockholders' reserves at the start of the comparative reporting period to restate the opening equity to the amount that would be arrived if the new accounting policy had always been applied.

Effect of Correction of Prior Period Error

The effect of correction of prior period errors must be presented separately in the statement of changes in equity as an adjustment to opening reserves. The effect of the corrections may not be netted off against the opening balance of the equity reserves so that the amounts presented in current period statement might be easily reconciled and traced from prior period financial statements.

Restated Balance

This represents the equity attributable to stockholders at the start of the comparative period after the adjustments in respect of changes in accounting policies and correction of prior period errors as explained above.

Changes in Share Capital

Issue of further share capital during the period must be added in the statement of changes in equity whereas redemption of shares must be deducted therefrom. The effects of issue and redemption of shares must be presented separately for share capital reserve and share premium reserve.

Dividends

Dividend payments issued or announced during the period must be deducted from shareholder equity as they represent distribution of wealth attributable to stockholders.

Income / Loss for the period

This represents the profit or loss attributable to shareholders during the period as reported in the income statement.

Changes in Revaluation Reserve

Revaluation gains and losses recognized during the period must be presented in the statement of changes in equity to the extent that they are recognized outside the income statement. Revaluation gains recognized in income statement due to reversal of previous impairment losses however shall not be presented separately in the statement of changes in equity as they would already be incorporated in the profit or loss for the period.

Other Gains & Losses

Any other gains and losses not recognized in the income statement may be presented in the statement of changes in equity such as actuarial gains and losses arising from the application of IAS 19 Employee Benefit.

Closing Balance

This represents the balance of shareholders' equity reserves at the end of the reporting period as reflected in the statement of financial position.

Purpose & ImportanceStatement of changes in equity helps users of financial statement to identify the factors that cause a change in the owners' equity over the accounting periods. Whereas movement in shareholder reserves can be observed from the balance sheet, statement of changes in equity discloses significant information about equity reserves that is not presented separately elsewhere in the financial statements which may be useful in understanding the nature of change in equity reserves. Examples of such information include share capital issue and redemption during the period, the effects of changes in accounting policies and correction of prior period errors, gains and losses recognized outside income statement, dividends declared and bonus shares issued during the period.

The official name for the cash flow statement is the statement of cash flows. We will use both names throughout AccountingCoach.com.

The statement of cash flows is one of the main financial statements. (The other financial statements are the balance sheet, income statement, and statement of stockholders' equity.)

The cash flow statement reports the cash generated and used during the time interval specified in its heading. The period of time that the statement covers is chosen by the company. For example, the heading may state "For the Three Months Ended December 31, 2015" or "The Fiscal Year Ended September 30, 2015".

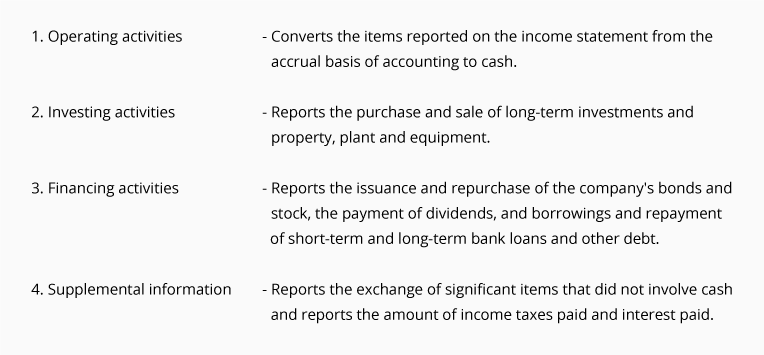

The cash flow statement organizes and reports the cash generated and used in the following categories:

To experience another presentation and to enhance your retention of the cash flow statement see AccountingCoach PRO for our visual tutorial, business forms to assist in preparing the statement, and exam questions.

What Can The Statement of Cash Flows Tell Us?Because the income statement is prepared under the accrual basis of accounting, the revenues reported may not have been collected. Similarly, the expenses reported on the income statement might not have been paid. You could review the balance sheet changes to determine the facts, but the cash flow statement already has integrated all that information. As a result, savvy business people and investors utilize this important financial statement.

Here are a few ways the statement of cash flows is used.

Simply the Statement of Changes in Equity is the Income Statement that shows net profit or net loss, while Statement of cash flow explains the ability of an entity to generate cash.

Statement of cash flows shows, a) cash flows from operating activities, b) cash flows from investing activities, and, c) cash flows from financing activities.

Statement of changes in equity shows any change in equity value / structure including cash flows from financing activities (c above).

Do you need help in adding the right keywords to your CV? Let our CV writing experts help you.